Episode Transcript

[00:00:00] Speaker A: Foreign.

[00:00:02] Speaker B: Let's look at the, the contracting season then Mark. That's rolling up around the corner very soon for you. And just for anyone listening, the Trans Pacific contracting season tends to be negotiated around Q1. Mark might correct me here and then a lot of people on that trade, they're shipping under long term contracts, normally annual contracts, but it's not set in concrete. Exactly. But Mark, what's your strategy given how you just described the market at the moment on those inventories?

[00:00:29] Speaker C: Yeah, you're right. I mean most shippers, big shippers, are negotiated in Q1, typically May 1 start date for Trans Pacific, which is different to most other trades. I think we're going to be looking to lock in again at least 80% of the volume that we have into contract.

I do expect those volume forecasts to be slightly down now. I think demand in some sectors, some of the bigger shipper sectors will be down and that's going to mean probably slightly smaller contracts than we, we set up this year. But still we'll be targeting the partners that we've been working with, the big carriers that we've been trying to improve post pandemic. We've been trying to improve relationships with the big carriers. That's going to be our focus and again, locking in the majority through contracts.

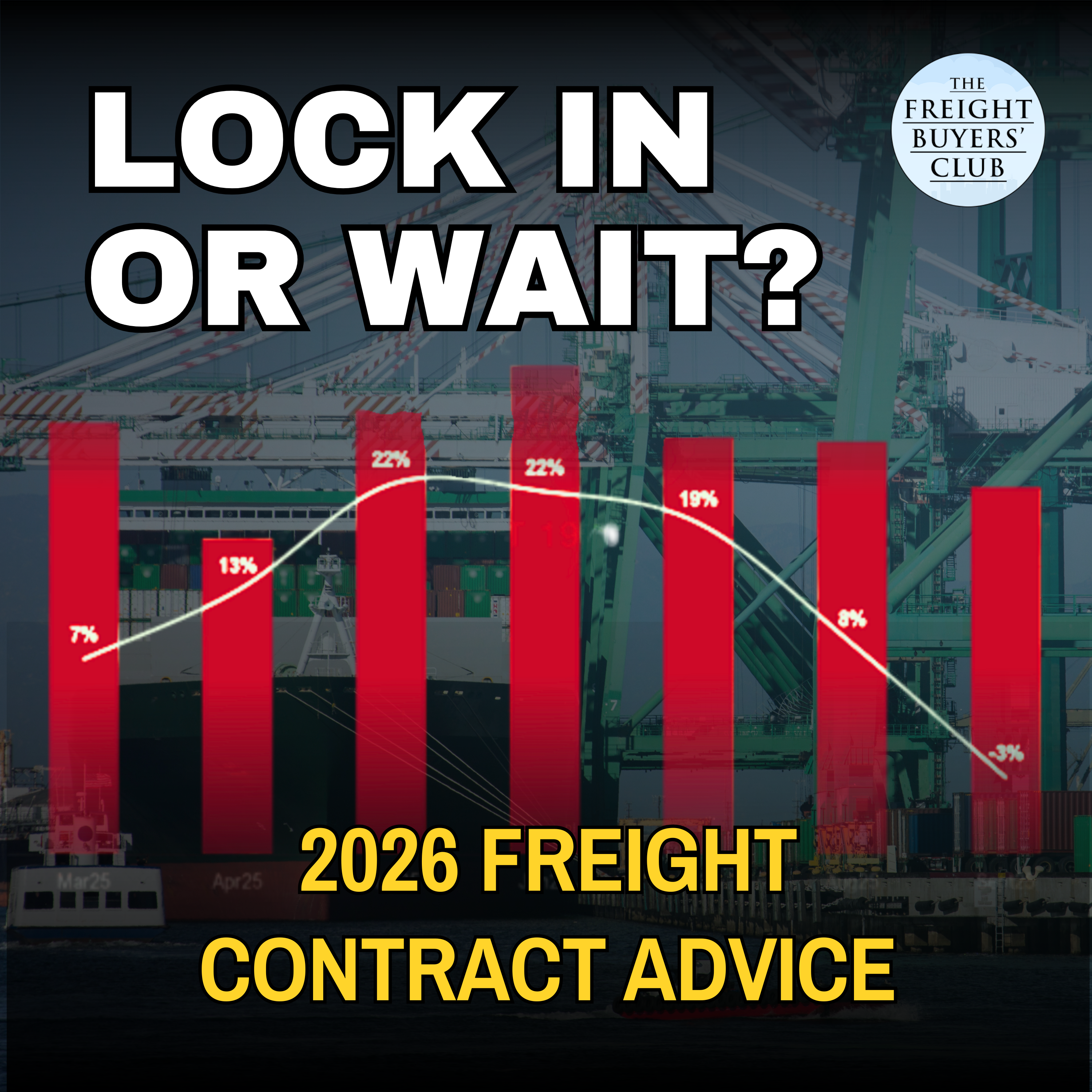

[00:01:16] Speaker B: Chantal, this is your specialist area, isn't it? Now for those watching, you should be able to see the Drury east west contract rate index which has been falling in line with spot rates.

So is this a buyer's market? Chantel, on the Trans Pacific? I mean, I'm assuming that you're going to say yes. So can you maybe give us some historical perspective via the previous years?

[00:01:36] Speaker A: So to answer the question, is it a buyer's market? I think it is if you have the cargo to ship. And remember, you know, the whole industry is dependent on demand.

So as long as we have the demand there and people have things to ship, it will become a buyer's market at Drury. When we're discussing the subject with shippers, we often refer to our supply and demand index because it's a fairly accurate barometer of what's going to happen with global freight rates in our world. Yacht 100 is the utopia. It's the perfect balance between supply and demand.

Carriers are making a reasonable profit and shippers are paying a reasonable ocean freight rate. And in that world, if you've ever seen it, everyone's however, we only either fluctuate way above a hundred or way below. So if I look back to 2019, the index was down to 84. So again, that was a buyer's market.

During COVID it shot back up to over a hundred. And we all know what happened then. 20, 23, it then dropped down to 77. So you can see what's happening here, the swings, the ups and downs. And then we had the Suez crisis, which really was the gift that the carriers needed to then get that sort of tightening of the gap between supply and demand to push the spot and the contract rates up. This year we're in a slightly different position. Our index is probably about 84, 85, and then we see it dropping 26, 27 and 28. So, you know, we're far, far away from that utopia where everybody is relatively happy with how the industry is moving forward. And at the moment, you know, with the index this low, it's heading towards record lows. It really will still be a buyer's market probably for the next three years.

[00:03:23] Speaker B: Okay, I'm going to, we're going to come back to the impact of peace in the Middle east if that's what we now have a bit later because that is critical for the overall global container shipping supply and demand balance. But we'll come back to that in a moment. Chantal, just in terms of how you would advise shippers to negotiate the market as it is now, obviously get those rates lower, but what else should they be thinking when they're committing volumes? Is this about reducing risk, improving resilience, better service? Please explain.

[00:03:54] Speaker A: It's definitely not on about rates this year. I think negotiating rates is the easy part. We work on bids with shippers and it's the first time I've seen seen carriers ask to get the rates in before the deadline. Everybody's rushing to get their homework in early, hoping for the best marks. It seems it's quite bizarre. And you know, if I'm advising a shipper, I'm now saying, go through your contracts with a fine tooth comb, start to focus on the other cost item and try and de risk those. So we're talking things like detention and demurrage. We all know that once the ocean crate goes down, the those costs become much more visible and people are always asked about them. So get ahead of the curve. You know, you can start to talk about things like payment terms as well. You can start to de risk the application of any additional surcharges during the course of the year. So I would be focusing on all of those and I would be having the conversations with my providers, whether it be carriers or forwarders, to make sure they understand that my contract has to be mutually beneficial because actually we need to work together to make this work. Service, on the other hand, is a tough one because that's ultimately delivered by the carriers and it's up to them really to treat their customers like customers, not just containers in a slot. So, you know, I think as a shipper, I'm going to be focusing on building mindset with my providers. I'm your customer. You deliver me a service, I will pay a reasonable rate for the service and I want, you know, reasonable terms and conditions around that. That's how I'd be approaching it this year.

[00:05:29] Speaker B: Mark, are the value add ons to price the type of thing that you look in this buyer's market that you're looking at for your customers when you're negotiating with carriers?

[00:05:41] Speaker C: Absolutely.

Everything that Chantal said, I think we see the same on our side over the last couple of years where. Well, a few years since COVID where as there's been this swing that was a little bit more favorable to the carriers, we've seen our contracts, some of the terms that we had have been lost. There've been some more punitive terms and conditions against shippers finding their way into contracts. I think it's time to take another look at that and say, okay, do these still make sense in this market? And it's not like flipping it in reverse and being punitive against the carriers. It's just finding a fair balance between. Between the two. So we are looking at those especially for the Trans Pacific. I think there'll be peak time to kind of reset the balance there. Get decent rates, but get some capacity locked in and get rid of some of these terms that are a little bit more punitive like detention, demoral agent and some of the free time that we've lost over the last few years.

[00:06:38] Speaker B: Have we seen any improvement in reliability? Well, we have for some of the carriers. Has there been a refocus? Because we had the Gemini cooperation launch this year. That's Maersk and Hapag Lloyd with this commitment to service reliability. Is this refocusing minds amongst carriers on service at all?

[00:06:56] Speaker C: Mark?

[00:06:56] Speaker B: I don't know. Or Chantal, if you want to go.

[00:06:59] Speaker C: I mean reliability I think is a big word in ocean freight.

If you move up from 60% reliable to 80% still pretty terrible for most manufacturers who are relying on tighter supply chains.

There's definitely been some improvement. How much of that is due to a dip in demand, an increase in capacity?

I think probably that's mostly what's improved. And what's changed. There's not really been too much else that we've seen.

[00:07:28] Speaker A: It's a really fine balancing act. I think the carriers are in quite a difficult position because you have to deliver reliability to become a preferred carrier to your shippers. But at the same time you have to manage your capacity. And one way they do that is with blank sailings which then of course impacts the schedule reliability.

And certain carriers have made big promises on hitting high levels of reliability.

So I really think that shippers can now sort of have those more structured conversations about listen, I'm not necessarily going to pay the lowest rate, but I do want the highest level of reliability. How do you make sure that I'm on the ship and I want to be on the ship and if I'm left behind that I'm first on the next one or to go to cancel daily. And I think, you know, vessel utilization is another thing that probably people need to start to look at because you know, if I look at the Transpac trade, its utilization is down to about 8, 80 to 85%. Last year it was 99%.

So you know, when utilization drops, profitability drops on these headhall trades and at that point they really need to start to break the capacity management which then meets schedule reliability drop. But then we come in this cycle of it and it's quite hard to break.

And we know that carriers haven't come up with a new idea as to do that. It's got kind of be going on a while now.

So you know, it begs the question who has the grand plan to break that?

[00:09:03] Speaker B: So. Well, I was going to ask you what's carrier strategy on the trans pack, but I think the answer is probably loads of blank sailings. If we're hitting 80% utilization, is that right?

[00:09:13] Speaker A: 80% utilization. If you haven't with blank sailings, if you've not made guarantees on schedule reliability 90.

That's, that's, that is the tricky part. If you are selling your service based on that and people are procuring based on that, then you kind of have to deliver. And actually Gemini has been doing it. Not that it hasn't, but instead of what do you know its competitors do to try and also keep their foot in the market as well.